[ad_1]

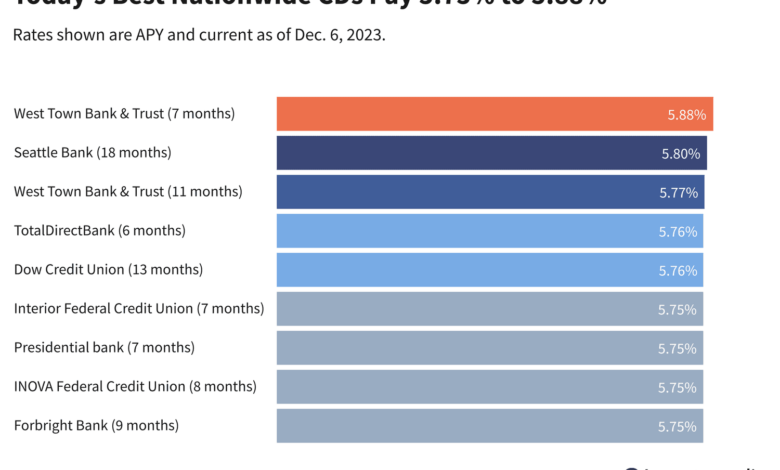

After a couple of days of losing CD term leaders, rates on the best nationwide CDs held their ground today. You can still earn 5.88% APY with the best-paying certificate in the country, and eight more options pay 5.75% or better—with terms ranging from 6 months to 18 months.

West Town Bank & Trust continues to wear our national rate crown, paying 5.88% APY on a 7-month term. Our runner-up is at the longer end of the spectrum: Seattle Bank’s 5.80% offer on 18 months. Meanwhile, the shortest-duration CD paying at least 5.75% APY is a 6-month certificate from TotalDirectBank.

Key Takeaways

- The top nationwide CD rate remains 5.88% APY, available for a 7-month term. For a longer 18 months, you can earn up to 5.80% APY.

- A total of 9 offers in our daily ranking of the best CDs pay 5.75% APY or better. They range in term from 6 to 18 months.

- The leading jumbo rate is 5.80% APY from All In Credit Union on an 18-month term.

- Markets overwhelmingly predict the Fed is finished with its rate increases, but Fed Chair Powell said more hikes could be on the table until inflation is reliably under control. CD rates are likely to flatten out, and eventually decline, unless the Fed raises rates again.

Below you’ll find featured rates available from our partners, followed by details from our complete ranking of the best CDs available nationwide.

If you’re looking for a nationwide CD paying a top rate of at least 5.75%, the longest duration available is 18 months, with Seattle Bank paying 5.80% on that term. But if you want to secure one of today’s historically high rates for longer, you can lock in 5.50% APY for either 2 years or 3 years.

Still not long enough? Though the leading 4-year rate fell this week, you can still snag 5.13% APY with a 48-month guarantee. Or if you can stretch to 5 years, you can secure a rate of 5.25% APY.

When asked in November if they were choosing more or less of certain investments during recent market events, 28% of Investopedia readers said they were leaning into CDs—the leading choice among more than a dozen options. Additionally, 14% of readers said they would open a CD if they had an extra $10,000 to invest, just behind the 15% who said they’d put it in individual stocks.

Jumbo CD rates have also seen a little shake-up this week. Through Friday, you could earn 5.85% on a 1-year jumbo certificate from two different institutions. Both of those offers evaporated earlier this week. In their wake, All In Credit Union has raised its 18-month jumbo rate to 5.80% APY, making that the current nationwide leader for jumbo-sized deposits.

Note that jumbo CDs don’t always pay a higher return than standard certificates. Sometimes you can do just as well—or better—with a standard CD. That’s currently the case in seven of the eight terms above, so it’s smart to shop both certificate types before making a final decision.

How High Will CD Rates Go This Year?

The Federal Reserve has been aggressively combating decades-high inflation since March of last year, raising the federal funds rate with fast and furious hikes in 2022 and then more moderate increases in 2023. This has created historically favorable conditions for CD shoppers, as well as for anyone holding cash in a high-yield savings or money market account.

The Fed opted to hold rates steady on Nov. 1, its second such move in as many meetings. That maintained the central bank’s benchmark rate at its highest level since 2001. But in his post-announcement press conference, Fed Chair Jerome Powell made it clear that holding rates in place right now does not necessarily mean the committee is finished with increases.

Since then, inflation data has come in encouragingly lower, down to its lowest rate since March 2021. As a result, financial markets increasingly predict the Fed will not make any further rate increases—including a 96% probability that the Fed will announce another rate hold on Dec. 13, according to the CME Group’s FedWatch Tool.

Still, Powell pushed back last week against predictions of rate cuts on the near-term horizon, indicating it’s premature to assume the Fed has concluded its rate-hike campaign. He said the committee is prepared to make yet another increase if it does not feel inflation has been sufficiently and reliably controlled.

As we always caution, trying to predict the Fed’s future rate moves is an uncertain exercise. But for now, it seems CD rates are likely to plateau near their current levels.

Note that the “top rates” quoted here are the highest nationally available rates Investopedia has identified in its daily rate research on hundreds of banks and credit unions. This is much different than the national average, which includes all banks offering a CD with that term, including many large banks that pay a pittance in interest. Thus, the national averages are always quite low, while the top rates you can unearth by shopping around are often five, 10, or even 15 times higher.

How We Find the Top CD Rates Today

Every business day, Investopedia tracks the rate data of more than 200 banks and credit unions that offer CDs to customers nationwide and determines daily rankings of the top-paying certificates in every major term. To qualify for our lists, the institution must be federally insured (FDIC for banks, NCUA for credit unions), and the CD’s minimum initial deposit must not exceed $25,000.

Banks must be available in at least 40 states. And while some credit unions require you to donate to a specific charity or association to become a member if you don’t meet other eligibility criteria (e.g., you don’t live in a certain area or work in a certain kind of job), we exclude credit unions whose donation requirement is $40 or more. For more about how we choose the best rates, read our full methodology.

Investopedia / Alice Morgan

Source link