[ad_1]

After performing poorly in 2022, growth stocks have largely rebounded this year, and some have far outshone the broader market’s solid performance. That was the case with e-commerce giant Shopify (NYSE: SHOP) and sports streaming specialist fuboTV (NYSE: FUBO). The former is up by 112% year to date, while the latter has risen by 95%.

However, these two stocks are unlikely to move in the same directions over the medium term; in fact, Shopify’s prospects look much brighter than fuboTV’s. Here’s why.

The case for Shopify

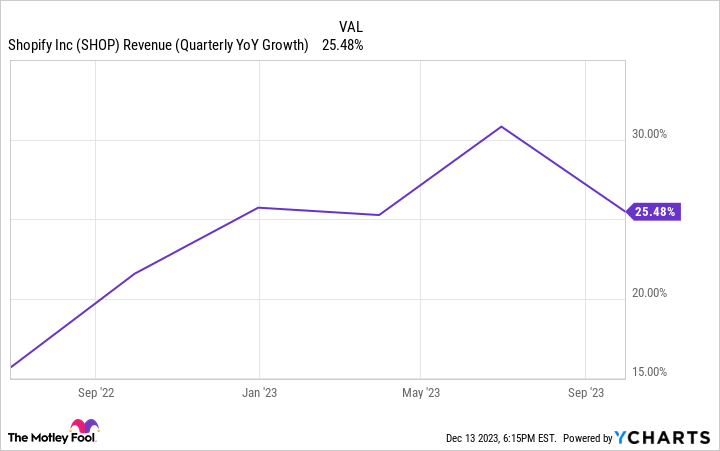

Shopify made important changes to its business this year. The company increased the prices of its services, which, together with a recovering economy, helped boost its revenue. In the third quarter, Shopify’s top line grew by 25% year over year to $1.7 billion. That was on the high end of the revenue growth rates it has recorded in the past year and a half.

However, another change may have an even more significant impact on Shopify. The company sold its logistics business to privately held Flexport in exchange for equity in the company. The move freed up a substantial amount of cash flow that Shopify will be able to dedicate to improving its core e-commerce operations while decreasing its expenses and improving its margins. Considering that the company still isn’t consistently profitable, it’s unsurprising that this move pleased investors.

The divestiture of its logistics arm helped boost Shopify’s gross profit by 36% year over year to $901 million in the third quarter, and its gross margin of 52.6% was much better than the prior-year period’s 48.5%. Its results could keep on improving next year along with the economy. Increased consumer discretionary spending should benefit the online merchants it serves and, by extension, Shopify itself. However, it’s the company’s long-term prospects that matter most.

On that front, Shopify continues to look attractive. This isn’t just because it has become the leader in its niche of providing businesses with all the tools they need to create killer online storefronts, along with key functionalities that let them sell their products across various social media platforms, among many other perks. One of the keys to Shopify’s future is its widening economic moat.

The company benefits from high switching costs since building (or rebuilding) an online store from scratch takes time and money. Clients could migrate to one of Shopify’s competitors, but it’s hardly worth the trouble. Further, Shopify’s brand has become intimately linked with the services it offers. These are powerful competitive edges that should allow the e-commerce specialist to grow its client base and its revenue. There remains a massive volume of white space in e-commerce.

The industry is projected to grow through the end of the decade and likely beyond. Shopify could benefit from that expansion while delivering market-beating returns on the way.

The case against fuboTV

FuboTV is one of many somewhat notable brands in the highly competitive streaming industry. Although it focuses much of its effort on covering the market for live sports, it offers plenty of other content. Its third quarterly results looked great, at least on the surface. Revenue increased by almost 43% year over year to $320.9 million. The company ended the period with 1.477 million subscribers in North America, an increase of 20% year over year.

That was in addition to solid increases in international subscribers and average revenue per user. FuboTV even boosted its full-year guidance. It now expects revenue of between $1.319 billion and $1.324 billion, which would amount to an increase of 34% at the midpoint. Management had previously been guiding for revenue in the $1.260 billion to $1.280 billion range.

That sounds great, but here’s what’s wrong with fuboTV’s business. In the third quarter, the company’s subscriber and related expenses (the money it pays to get the rights to show the content it does) came in at $286.1 million, up about 33% year over year and almost as high as its subscription revenue of $289.6 million (fuboTV also makes money from advertising and other sources).

This single category of expenses gobbles up almost all of fuboTV’s subscription revenue — its largest source of sales by far. And that has been the story with the company for a while. As a result, fuboTV’s gross margins are razor thin, and the company is deeply unprofitable on an operating expense basis. Further, its subscription business can be seasonal, as fans of specific sports often cancel the service during their off-seasons.

In addition, it’s hard to say that fuboTV has a competitive advantage. Plenty of other streaming leaders are battling with it in the world of sports, and some have much deeper pockets and are better able to handle subscriber-related costs. That puts it in a difficult position. While the streaming industry should continue flourishing in terms of overall viewership and streaming hours, it’s not clear that fuboTV will deliver the kind of top-line growth it needs to consistently become profitable even on an operating basis anytime soon, despite the progress it made this year.

That’s why investors should stay away from this growth stock.

Should you invest $1,000 in Shopify right now?

Before you buy stock in Shopify, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Shopify wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 7, 2023

Prosper Junior Bakiny has positions in Shopify. The Motley Fool has positions in and recommends Shopify and fuboTV. The Motley Fool has a disclosure policy.

1 Growth Stock to Buy Ahead of 2024, and 1 to Avoid was originally published by The Motley Fool

Source link