[ad_1]

(Bloomberg) — For some, a slump of almost 60% is a signal to buy Chinese stocks.

Most Read from Bloomberg

Almost a third of 417 respondents to Bloomberg’s latest Markets Live Pulse survey say they will increase their China investments over the next 12 months. That compares with just 19% in a similar August survey and is higher than the 25% who planned to boost exposure in March. Only a fifth now anticipates cutting their China holdings.

Chinese stocks peaked in early 2021 and have since slumped almost 60% to be languishing in a bear market, according to the MSCI China Index. The decline reflects a real estate debt crisis, eroding consumer confidence and China’s slowing economy. Now, the country’s stocks are among the world’s cheapest relative to their profits.

Some investors, including Invesco Ltd. and Pzena Investment Management, are beginning to take note.

“China is a market that is out of favor so that enables us to buy stocks relatively cheap,” said Vivek Tanneeru, an portfolio manager for Matthews Asia in San Francisco. Tanneeru has overweight positions in Chinese stocks in the two emerging markets portfolios he oversees.

Relative 2023 outperformance in markets like India and Brazil means allocations to China sit near decade lows, recent Goldman Sachs Group Inc. research showed. Separate survey data from Bank of America Corp. showed China was also the most underweighted Asian market. That means there’s more room to increase rather than cut allocations.

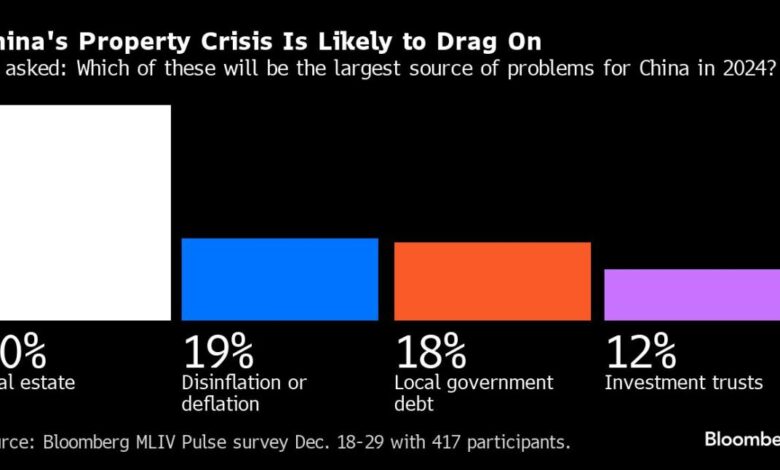

Betting on China is not without considerable risk. The country’s property sector is still in a slump, weighing on confidence across the economy. It is expected be the biggest source of problems for China in 2024, the MLIV Pulse survey showed.

“The elephant in the room is the real estate market,” said Alejandra Grindal, chief economist for Ned Davis Research. “The number one household asset is houses — that’s where the majority hold their wealth. If it is not increasing, that acts as a drag on confidence.”

The potential for swift change in China that can hammer corporate profits — and by extension, equity valuations and creditworthiness — was again on display in late December when officials announced draft rules capping time and money spent on online gaming. Beijing signaled considerations to soften its stance after a sudden plunge in some of China’s biggest companies.

The persistent selling in Chinese stocks has detached prices from fundamentals, according to Nicholas Ferres, chief investment officer for Vantage Point Asset Management in Singapore.

“The third consecutive negative year for China suggests ‘revulsion’,” Ferres said, employing a term that captures the broad distaste for the country’s equities that can act as a contrary buying signal. His fund added to positions in Chinese tech stocks in October.

Cheap valuations, however, have failed to be enough of a reason to buy Chinese stocks in the recent past. Triggers for the MSCI China to rally could include some form of Chinese-style quantitative easing, according to the MLIV Pulse survey, as well as more stock purchases by government-backed funds.

“One potential upside surprise for China is if the government engaged in some sort of fiscal support for households because that is the part of the economy that continues to see weakness,” said Grindal of Ned Davis Research. “You need to see momentum accelerate for a period of time because investors have been burned in the past.”

Other potential triggers include a tangible improvement in consumer confidence and a softening of geopolitical tensions with the US.

After a painful 2023 for Chinese markets, the hope is that 2024 will be different. But should investors continue to shy away, almost half of MLIV Pulse respondents say India will be the most likely to benefit, followed by Southeast Asia. Ferres disagrees, anticipating Indian shares to underperform in 2024 relative to Chinese stocks given the two markets’ divergence.

The price-to-earnings ratio based on expected profits for Chinese companies sits below 10 — almost half the global average and well below the ratios commanded by Indian stocks, according to MSCI indexes. Investor demand for Indian equities as a source of growth in emerging market portfolios pushed prices on Mumbai’s bourse 19% higher in 2023.

The MLIV Pulse survey was conducted among Bloomberg readers in the final two weeks of 2023 by Bloomberg’s Markets Live team, which also runs the MLIV blog. This week, the survey focuses on the earnings season. Do you think the S&P 500 earnings expectations for 2024 are too high or too low? Share your views.

Most Read from Bloomberg Businessweek

©2024 Bloomberg L.P.

Source link