[ad_1]

Top Canadian cannabis producer Tilray Brands (NASDAQ: TLRY) recently reported earnings. But despite the record sales numbers, the stock hasn’t been soaring in value. Instead, it has been falling in recent days following the release of the company’s earnings. Here’s a closer look at why investors haven’t been rushing to buy the stock.

A sales boost helped by recent acquisitions

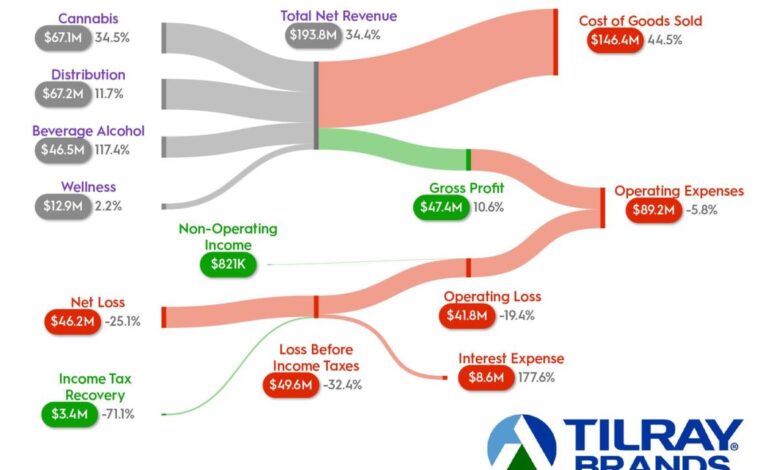

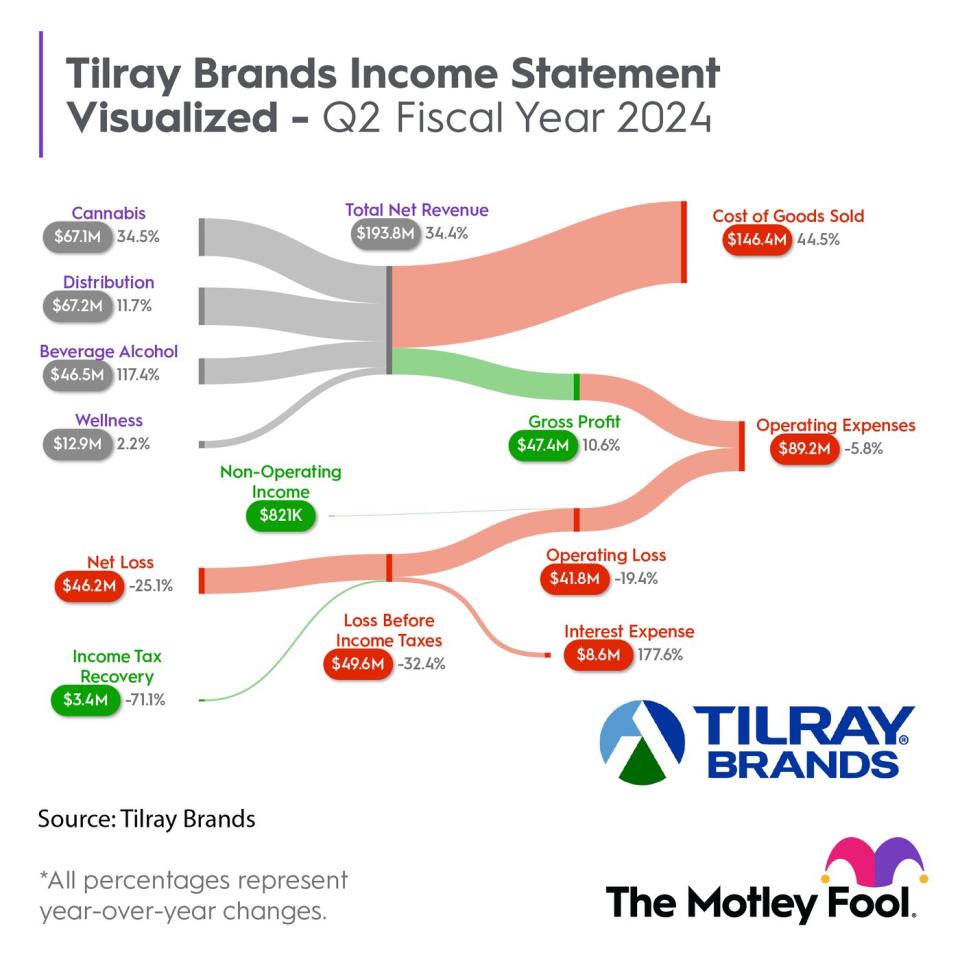

For the second quarter of Tilray’s fiscal 2024, which ended Nov. 30, 2023, the company reported net revenue of $193.8 million, up 34% from a year ago. Many cannabis producers have been struggling to generate meaningful year-over-year growth, and so that is definitely a positive for Tilray.

But the stronger top-line results were largely due to acquisitions; within the past year, the company has closed on multiple transactions, including that of rival cannabis producer Hexo. In October, it also acquired eight beverage brands from beer giant Anheuser-Busch as it looks to strengthen its presence in the U.S. craft beer market, where it is now the fifth-largest craft brewer.

While the company did generate good revenue growth, its gross profit only increased by 11%; intense competition in the Canadian cannabis market makes it difficult for producers to generate strong margins. Tilray’s gross margin was actually higher for beverages (34%) last quarter than it was for cannabis (31%). The company’s net loss did shrink from $61.6 million in the prior-year period to $46.2 million, but breakeven remains nowhere in sight.

Tilray’s troubling cash burn

What’s arguably most important for cannabis companies these days is cash flow. If a growing company isn’t generating enough cash, then dilution becomes a significant risk for investors.

Last quarter, Tilray used up $30.4 million in cash to fund its day-to-day operating activities. A year ago, its quarterly cash flow was a positive $29.2 million. Although there have been periods where Tilray’s cash flow has been positive, cash burn remains an ongoing problem.

The company’s cash and cash equivalents balance as of the end of the period totaled $143.4 million. Tilray isn’t in a dire need of raising money right now but with the company seeming to have an appetite for acquisitions and growing its operations in both Canada and the U.S., the risk of dilution, whether it’s due to cash burn or funding other acquisitions, does appear high.

Tilray does expect to generate positive free cash flow in fiscal 2024 (which ends on May 31), but that’s on an adjusted basis.

Is Tilray’s stock a buy?

These latest results don’t give cannabis investors much of a reason to invest in Tilray. The company was able to generate revenue growth but its numbers would have looked less impressive without recent acquisitions. Meanwhile, its modest gross profit margin and cash burn are still concerning issues that investors shouldn’t ignore. While the company has been diversifying into alcohol, this is still a business that faces a lot of challenges ahead.

Shares of Tilray have declined 82% over the past three years, and there isn’t much of a reason to expect a big turnaround soon as getting to breakeven won’t be easy, nor will generating positive cash flow. And until both of those things happen, investors are better off avoiding the stock.

Should you invest $1,000 in Tilray Brands right now?

Before you buy stock in Tilray Brands, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Tilray Brands wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 8, 2024

David Jagielski has no position in any of the stocks mentioned. The Motley Fool recommends Tilray Brands. The Motley Fool has a disclosure policy.

Tilray Brands Just Posted Record Revenue, but Here’s Why Investors Aren’t Impressed was originally published by The Motley Fool

Source link