[ad_1]

Dividend stocks don’t have to be boring. Some can really spice up your portfolio by providing diversification, extra income potential, or a supercharged yield.

In that category, Franco-Nevada (NYSE: FNV), Diamondback Energy (NASDAQ: FANG), and Energy Transfer (NYSE: ET) stand out to a few Fool.com contributors as strong contenders to enhance any dividend stock portfolio.

All that’s gold doesn’t glitter

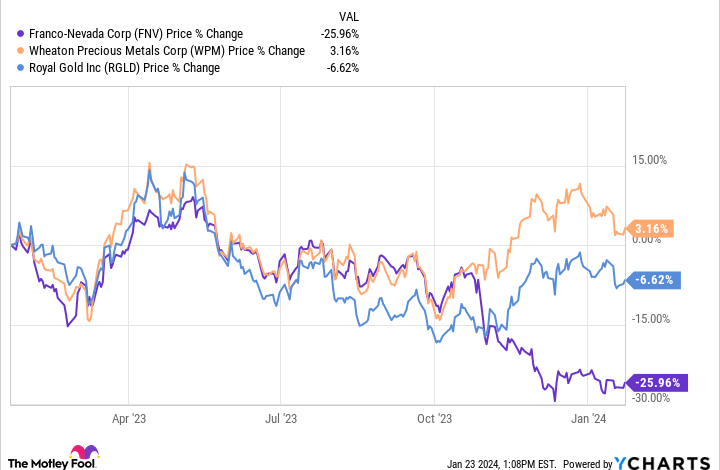

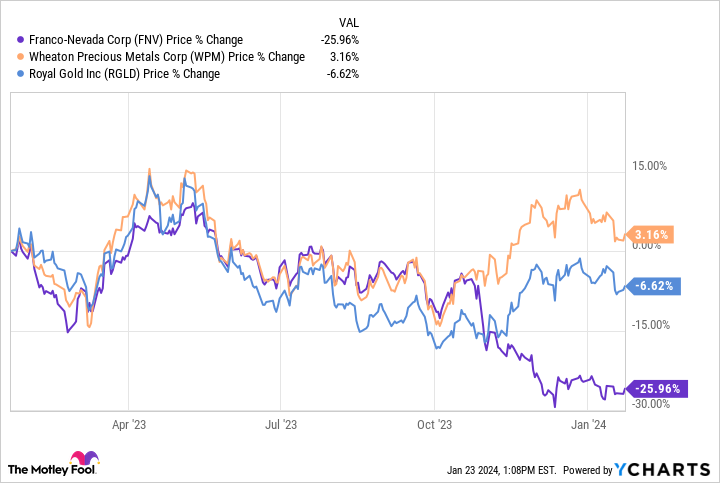

Reuben Gregg Brewer (Franco-Nevada): As a streaming and royalty company, Franco-Nevada provides cash up front to mine operators in exchange for the right to buy gold and other precious metals from them at reduced rates in the future. It is best to think of such companies as managing portfolios of mine investments. Right now, though, Franco-Nevada’s largest investment is, effectively, shut down. That explains why the stock is drastically underperforming its closest peers, which has pushed its yield up toward its highest levels in five years.

There’s going to be some uncertainty around the company’s business for a little while, but management is confident that the situation at the shuttered Cobre Panama mine will be worked out equitably in time. That’s not based on hopes and dreams: Management has seen similar situations in the past. However, thanks to the concern around this mine’s future, dividend investors can buy Franco-Nevada at what appears to be a very attractive price, historically speaking.

Here’s the problem. The yield is only 1.2%. But the company has increased its payout annually for 16 years, which income investors should find appealing. And, here’s the really important fact: It’s a way to buy a reliable dividend stock that also adds the diversification benefits of precious metals to your portfolio. In other words, Franco-Nevada allows you to own a gold company without having to forgo your broader dividend approach.

The potential to pay a high-octane dividend

Matt DiLallo (Diamondback Energy): Diamondback Energy can really add some spice to your dividend portfolio. It has increased its base dividend payout at a blistering 9% average quarterly rate since its inaugural payment in 2018. The oil producer gave investors two raises last year, boosting its payout by 7% in February and another 5% in July. The current base rate of $0.84 per quarter ($3.36 annually) gives Diamondback a 2.2% dividend yield at its current share price — exceeding the S&P 500‘s 1.5% yield.

That above-average and steadily rising base payment is pretty tasty on its own. However, Diamondback Energy really amps things up with the other part of its payout — its variable dividend. For example, it paid a $2.53 per share variable dividend in the third quarter. The total payment was a monster 300%-plus increase from the second quarter’s level. That gave Diamondback an 8.3% annualized dividend yield at the time.

The problem with those variable payouts is that they fluctuate from quarter to quarter based on the company’s oil-fueled cash flows and its flexible return of capital program. Diamondback aims to return 75% of its free cash flow to investors each quarter. While the base dividend takes priority, Diamondback can also return cash to shareholders through stock repurchases and variable dividends. Due to market conditions, it limited its stock buybacks in the third quarter and paid a higher variable dividend instead. However, it has prioritized repurchases in the past. (Indeed, it didn’t pay any variable dividend in the second quarter because it used all its excess free cash to buy back shares.)

At a minimum, Diamondback Energy pays an above-average and steadily rising base dividend. However, it has the potential to add some zest through variable dividends, making it an exciting option for your dividend portfolio.

Slow but steady

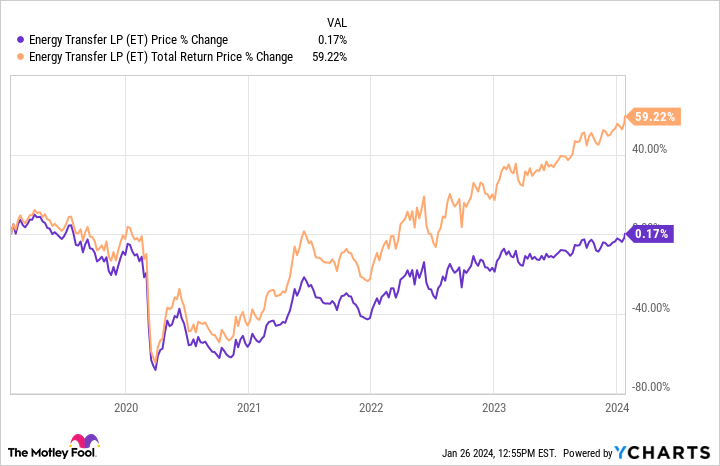

Neha Chamaria (Energy Transfer): Energy Transfer, which yields 8.7% at its current share price, is a great dividend stock to add to your portfolio now, given the midstream energy giant’s commitment to grow its payouts while investing in its business.

Management is targeting an annual dividend growth rate of 3% to 5%, and wants to pay out more than half of its distributable cash flow as dividends. That’s an achievable goal, considering how Energy Transfer has been growing steadily through organic projects and acquisitions. Last year alone, the company made two important purchases, one of which was Crestwood Equity Partners, which it bought for $7.1 billion. That acquisition, completed in November, gave Energy Transfer entry into the Powder River Basin, and was immediately accretive to Energy Transfer’s distributable cash flow per unit. That should only make its dividend growth goal even more sustainable.

On Jan. 25, Energy Transfer announced a 3.3% hike to its payout. That may not sound much, but the master limited partnership’s dividend growth has contributed significantly to shareholder returns in recent years and will likely continue to do so.

Energy Transfer has a balanced asset mix and is spreading its investments across all of its asset categories, including midstream gathering and processing, crude oil, natural gas liquids and refined products, and interstate transport and storage. With the company also adopting a balanced capital allocation policy that prioritizes dividends and investments in growth while maintaining a manageable balance sheet, investors can rely on this stock for steady extra income.

Should you invest $1,000 in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 22, 2024

Matthew DiLallo has positions in Energy Transfer. Neha Chamaria has no position in any of the stocks mentioned. Reuben Gregg Brewer has positions in Franco-Nevada. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

3 Great Dividend Stocks to Spice Up Your Portfolio was originally published by The Motley Fool

Source link