[ad_1]

Quality growth stocks have the potential to deliver outsized gains to long-term shareholders, especially during bull markets. It’s essential to consistently identify companies growing at a higher pace compared to the overall market to benefit from massive upside potential over time.

Most growth stocks trade at a premium, as investors expect a steep increase in revenue and earnings, which eventually translates to a higher valuation.

One such mid-cap growth stock is e.l.f. Beauty (NYSE:ELF) has already delivered outsized gains to shareholders in the last five years. e.l.f. Beauty has surged over 1,800% since January 2019 and is trading near all-time highs.

Despite its market-beating gains, I expect the stock to deliver robust returns in the upcoming decade as I am bullish on the company’s widening competitive moat, strong earnings growth, and recession-resistant business.

An Overview of e.l.f. Beauty

Valued at $8.8 billion, e.l.f. Beauty offers a portfolio of cosmetic and skin care products to consumers globally. These products are sold through a network of national and international retailers as well as direct-to-consumer.

e.l.f. has a family of brands that include e.l.f. Cosmetics, e.l.f. SKIN, Well People, and Keys Soulcare. These brands can be purchased online or across leading mass market and specialty retailers such as Walmart (NYSE:WMT), Target (NYSE:TGT), and Ulta Beauty (NASDAQ:ULTA), allowing the company to expand distribution in the U.S. and other international markets.

Its high-quality products have a universal appeal, especially among millennials and the Gen Z demographic.

A Customer-Centric Marketing Model

e.l.f. Beauty has deployed a consumer-centric marketing model, as the company has focused on building brand equity by driving traffic to its e-commerce platform and retail partners through digital and social media.

Comparatively, legacy cosmetic brands acquire customers through traditional media, such as celebrity endorsements, television ads, and magazines.

In Fiscal 2023 (ended in March 2023), e.l.f. Beauty spent $126 million on marketing, which accounted for 22% of its net sales. Several of its customers active on social media write product reviews online and generate content on platforms such as Instagram, TikTok, and YouTube, creating a social media flywheel for e.l.f. Beauty in the process.

A Focus on the Supply Chain

e.l.f. Beauty has successfully developed a scalable and asset-light supply chain. Its products are sourced and manufactured in China in collaboration with a network of third-party manufacturers.

e.l.f. Beauty emphasizes its broad supply base provides it with the ability to fulfill product requirements and remain cost-competitive as it continues to work with suppliers on product innovation and quality.

It has two main distribution centers in California that serve national retail customers, while another distribution center in Ohio serves e-commerce demand. Further, these distribution centers are operated by a leading third-party logistics provider. It also uses third-party logistics partners in Canada and the UK to distribute products in certain international markets. e.l.f. has invested heavily in capital expenditures to automate its processes, driving its costs lower.

How Did e.l.f. Beauty Perform in Fiscal Q2 2024?

e.l.f. Beauty reported revenue of $215.5 million in Fiscal Q2 2024, an increase of 76% year-over-year. Its top-line growth was driven by strong sales in retail and e-commerce channels.

The company reported a gross margin of 71% in Q2, up from 65.3% in the year-ago period, due to lower inventory, cost savings, a strong U.S. dollar, and improved transportation costs. Its operating expenses rose at a much lower pace to $112.2 million, accounting for 52% of net sales.

e.l.f. Beauty reported an adjusted net income of $47.1 million or $0.82 per share in Q2, compared to a net income of $20 million or $0.36 per share in the year-ago period. Its adjusted EBITDA (earnings before interest, tax, depreciation, and amortization) more than doubled to $60.4 million in Q2, indicating a margin of 28%.

e.l.f. Beauty ended the quarter with $167.8 million in cash and $57.7 million in long-term debt. Its improving profit margins have enabled e.l.f. Beauty to roughly double its balance sheet cash in the last 12 months, providing it with the flexibility to reinvest in growth and target accretive acquisitions. For instance, e.l.f. Beauty closed the acquisition of Naturium, a high-performance skincare brand, last October for $355 million.

Its stellar performance in Q2 and the above-mentioned acquisition meant e.l.f. Beauty now aims to end Fiscal 2024 with sales between $896 million and $906 million, much higher than its previous mid-point revenue guidance of $797 million.

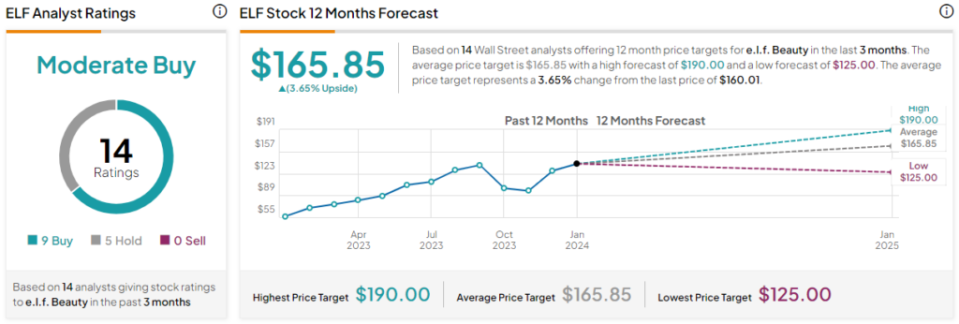

Is ELF Stock a Buy, According to Analysts?

Out of the 14 analysts covering ELF stock, nine recommend a Buy, five recommend a Hold, and none recommend a Sell, giving it a Moderate Buy consensus rating. The average ELF stock price target is $165.85, 3.7% above the current price.

Analysts also expect ELF stock to expand its adjusted earnings to $3.22 per share in Fiscal 2025, indicating a forward P/E of 49.7x, which is steep, given that the median multiple for this sector is much lower at 17.9x.

However, ELF stock is growing at a much faster pace compared to peers, allowing it to command a premium valuation.

The Key Takeaway

The personal cosmetics industry is fairly recession-resistant, which should enable e.l.f. Beauty to enjoy predictable cash flows across market cycles. A lower cost base should also translate to higher margins for the company once inflation cools down.

e.l.f Beauty is a digitally disruptive brand with massive upside potential, given that it’s yet to gain traction in emerging economies, making it a compelling investment today.

Source link