[ad_1]

(Bloomberg) — Private equity firms that amassed more than $1.5 trillion of assets in China in just two decades are now struggling to offload once-promising investments they were counting on for hefty returns.

Most Read from Bloomberg

With public markets in a slump and offering unattractive valuations, buyout firms are exploring private sales. But mounting concerns about the risks of investing in mainland China have left so-called secondary buyers demanding discounts of 30% to more than 60%, according to people familiar with the market. Haircuts in Europe and the US are closer to 15%.

Many firms are also looking at an alternative strategy, putting off sales by setting up so-called continuation funds to take over holdings for several more years, according to interviews with about a dozen of private equity investors and advisers. That’s also proving challenging.

The lack of easy exits — affecting the likes of Blackstone-backed PAG and Carlyle Group Inc. — has shifted the world’s second-largest economy from a vast frontier for buyouts into an uncertain landscape for long-term investing. Demand for Chinese assets cratered in the past few years, with record outflows even from public markets, as the economy struggles to regain traction and concerns mount over the political direction under Xi Jinping.

“We are in more challenging times, very similar to the way we experienced the global financial crisis,” said Niklas Amundsson, partner at Monument Group, a global private placement agent. “China is completely out of favor and global investors are going to put China on hold for now.”

Fresh Capital

Hong Kong-based PAG, which oversees $50 billion and focuses on Asia, has been trying for a few months to arrange a tender offer for about $1 billion of assets in prior funds, people familiar with the matter, including potential buyers and their advisers, have said, asking not to be named discussing confidential talks. A spokesperson declined to comment.

Some transactions may proceed thanks to the right conditions.

Carlyle Group and Trustar Capital have been seeking a partial exit for their investment in McDonald’s Corp.’s operations in Hong Kong and China — a potential $4 billion deal that could involve setting up a new vehicle while attracting fresh capital, people with knowledge of the talks have said.

The key difference in that case is that the company’s earnings are robust, making a partial private cash-out of the aging investment more feasible, even if a public offering isn’t attractive in the current environment. A final agreement and terms have yet to be set.

Spokespeople for Carlyle and Trustar declined to comment.

Fundraising Slump

It’s a tough time all around for private equity.

After years of growth, some institutional clients, such as US pension systems, have reached the limit of what they’re willing to allocate to the sector, making it all the harder for small- and mid-sized money managers to raise fresh funding in an era of rising interest rates. Secondary buyers are finding it increasingly challenging to price risk. Some would be-clients also privately harbor reservations about the quality of some Asia PE firms and their assets, the people said.

Deals in China involving private equity firms are on track to slide for a second straight year, after plunging by 50% last year, according to data compiled by Bloomberg.

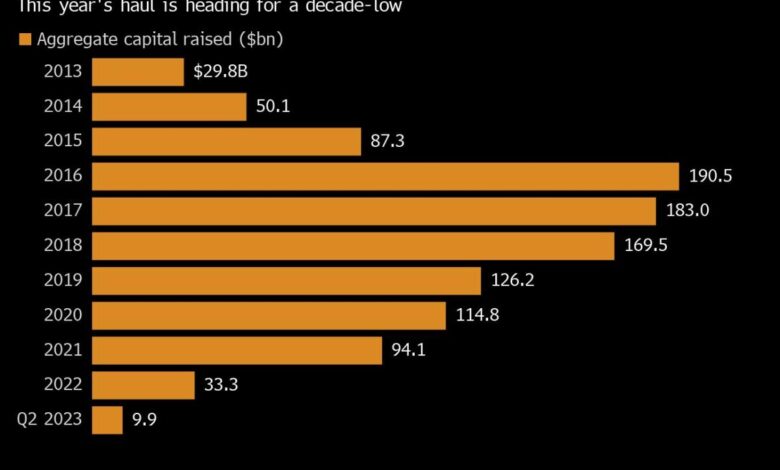

Some 151 funds targeting the greater-China region collectively raised $33.3 billion last year, the industry’s smallest haul since 2013, according to Preqin. This year looks even bleaker.

Meanwhile, difficulties with valuations and exits have led to an increase in dry powder, which stood at $216 billion at the end of 2022.

Clients are showing more interest in funding deals in other parts of the region, such as India, Vietnam, South Korea, Australia and Japan. The US, where returns have leapfrogged those in Asia, is the preferred destination, the people said.

For funds started in 2021, average returns on US investments amounted to 11.2%, based on cash flows of portfolio companies, according to a March 31 report by Cambridge Associates seen by Bloomberg. That compares to 6.1% for emerging-market funds mostly focusing on Asia-Pacific.

Survivors’ Strength

International investors can’t afford to ignore opportunities in China altogether, Citadel founder Ken Griffin told a conference in Hong Kong last week. They have “got to be watching and investing here in China.”

Indeed, Hillhouse is looking. The Asia-based firm became a juggernaut by presciently investing money from Yale University’s endowment decades ago in companies that became some of China’s largest. It’s been gauging international investor interest for what is expected to be a multibillion-dollar fund to buy beaten-down Chinese firms.

“The best companies are built in the worst, challenging times,” Chairman Zhang Lei, founder of the $80 billion investment house, said at the Hong Kong conference. “You’re going to see the greatest companies in the making in this period of time.”

Others have explored bets. Blackstone Inc., is considering a potential acquisition of Growatt Technology Co. that could value the Chinese solar equipment maker at about $1 billion, people with knowledge of the matter said in September. Ascendent Capital Partners, a China-focused private equity firm, has made a $1.6 billion takeover bid for Hollysys Automation Technologies Ltd.

But in the short term, at least, pessimism keeps creeping into the conversation.

Yichen Zhang, the chief executive officer of Trustar Capital, the private equity affiliate of Citic Capital Holdings, said last week it will take time to wean China’s economy off real estate. Meanwhile, he sees a tough year ahead there with fundraising still very tight.

Most Read from Bloomberg Businessweek

©2023 Bloomberg L.P.

Source link