[ad_1]

Calculate monthly payments for different loan scenarios with our Mortgage Calculator.

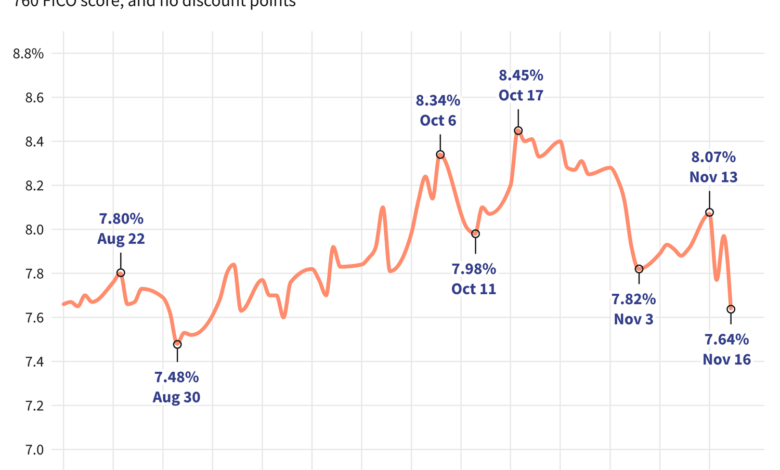

The rates you see here generally won’t compare directly with teaser rates you see advertised online, since those rates are cherry-picked as the most attractive, while these rates are averages. Teaser rates may involve paying points in advance, or they may be selected based on a hypothetical borrower with an ultra-high credit score or taking a smaller-than-typical loan. The mortgage rate you ultimately secure will be based on factors like your credit score, income, and more, so it may be higher or lower than the averages you see here.

Lowest Mortgage Rates by State

The lowest mortgage rates available vary depending on the state where originations occur. Mortgage rates can be influenced by state-level variations in credit score, average mortgage loan type, and size, in addition to individual lenders’ varying risk management strategies.

The states with the lowest 30-year new purchase averages were Vermont, Delaware, North Carolina, Tennessee, and Alaska, while the states with the highest averages were Oregon, Nevada, Arizona, Minnesota, and Washington.

What Causes Mortgage Rates to Rise or Fall?

Mortgage rates are determined by a complex interaction of macroeconomic and industry factors, such as:

- The level and direction of the bond market, especially 10-year Treasury yields

- The Federal Reserve’s current monetary policy, especially as it relates to bond buying and funding government-backed mortgages

- Competition between mortgage lenders and across loan types

Because fluctuations can be caused by any number of these at once, it’s generally difficult to attribute the change to any one factor.

Macroeconomic factors kept the mortgage market relatively low for much of 2021. In particular, the Federal Reserve had been buying billions of dollars of bonds in response to the pandemic’s economic pressures. This bond-buying policy is a major influencer of mortgage rates.

But starting in Nov. 2021, the Fed began tapering its bond purchases downward, making sizable reductions each month until reaching net zero in March 2022.

Since that time, the Fed has been aggressively raising the federal funds rate to fight decades-high inflation. While the fed funds rate can influence mortgage rates, it does not directly do so. In fact, the fed funds rate and mortgage rates can move in opposite directions.

However, given the historic speed and magnitude of the Fed’s 2022 and 2023 rate increases—raising the benchmark rate 5.25 percentage points over the last 18 months—even the indirect influence of the fed funds rate has resulted in an upward impact on mortgage rates over the last two years.

The Fed has opted to hold rates steady at its last two meetings, which concluded Sept. 20 and Nov. 1. But Fed Chair Jerome Powell has made it clear that another rate increase is still possible at a future meeting. The Fed’s next rate announcement will be made Dec. 13.

Methodology

The national averages cited above were calculated based on the lowest rate offered by more than 200 of the country’s top lenders, assuming a loan-to-value ratio (LTV) of 80% and an applicant with a FICO credit score in the 700–760 range. The resulting rates are representative of what customers should expect to see when receiving actual quotes from lenders based on their qualifications, which may vary from advertised teaser rates.

For our map of the best state rates, the lowest rate currently offered by a surveyed lender in that state is listed, assuming the same parameters of an 80% LTV and a credit score between 700–760.

Investopedia / Alice Morgan

Source link